[ad_1]

The insurance industry is experiencing a growing talent shortage. While this challenge has been anticipated, much of the discussion on solutions is often generalized to the entire workforce. But not every job will be impacted in the same way. As insurers grow, some functions will need more support, while others will be better primed to use cognitive technology, like AI, RPA and more. This means some jobs will be replaced by technology, other jobs will be enhanced by technology and other jobs will require more humans (an area where people can shift to, if their job is replaced).

The fact is that insurance operations are changing, and people are the center of that change. The question isn’t, “How do we address this workforce gap?” The question is, “How will claims, underwriting and sales be impacted by this workforce gap, and how can we leverage technology to address each one to improve our operations holistically?” That’s what I’ll be exploring here.

Urgency needed to address the growing workforce gap in insurance

In June 2021, the US Chamber of Commerce released the The America Works Report with alarming statistics:

- Less than 25% of the insurance industry is under 35 years old.

- In the last 10 years, insurance professionals aged 55 and older increased by 74%.

- The Bureau of Labor Statistics estimates that over the next 15 years, 50% of the current insurance workforce will retire.

- There will be more than 400,000 open positions unfilled over the next decade.

These statistics paint a startling picture—and one that requires an urgent response. But an aging workforce isn’t the only concern:

- Insurance companies are also trying to grow, meaning they either need a larger workforce or the ability to scale with the current size workforce.

- Many times, there is a skills mismatch where the current insurance workforce lack the skills needed to operate in an automated and data centric environment.

- While insurance companies don’t always need hundreds of elite tech engineers, they do need their fair share of foundational and complimentary technical specialists, especially as the focus on AI/ML and the cloud continues to increase. This can create talent competition with big tech companies that offer higher salaries, more perks and more innovative work.

Tackling the workforce gap holistically

Realistically, the industry will not be able to replace 400,000 open positions one-to-one. And even if it did, the amount of knowledge loss with 50% of the workforce retiring is enormous. This is where cognitive technology comes in as part of the solution.

It’s important to emphasize that technology is only part of the workforce gap solution. While more administrative, redundant tasks can be automated, other functions may need more people (like sales-related areas, which I’ll explore in detail later).

Insurers need to do two contradictory things at the same time: Look at their workforce individually and holistically. Decision makers need to know the impact of the workforce gap and the supporting technologies for each individual job function. But since jobs don’t operate in silos (at least, they shouldn’t), insurers also need to have a holistic understanding of how changes will impact the way different functions interact with and support each other. Ultimately, there is no one-size-fits-all solution. But there are important insights for all insurers to consider.

Cognitive technology is changing the insurance workforce

Cognitive technology will impact different jobs in different ways. Some jobs will be replaced by automation; others will be augmented by technology; and other jobs will need to grow the human workforce in tandem with technology.

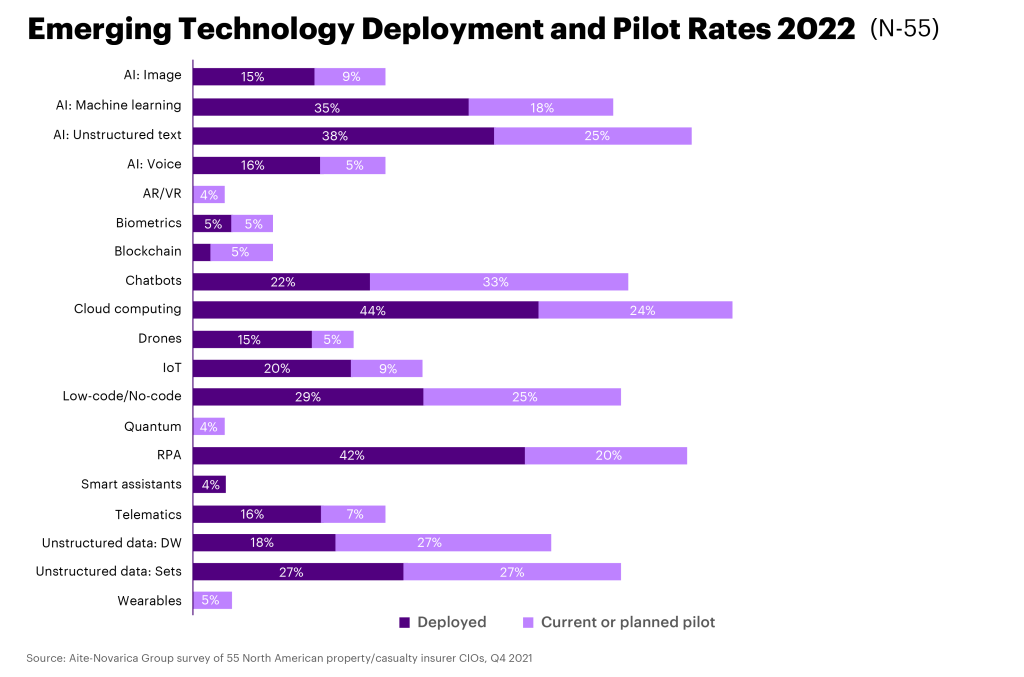

Before jumping into specific job functions, it’s important to understand the types of technology that are becoming more and more ubiquitous. The following table highlights the technology P&C insurers are focusing on in 2022.

Clearly, AI, data and RPA are major areas of focus. Chatbots are also being used more often to improve customer service, while cloud and data remain key areas for operational efficiencies and insights. Each of these technologies will impact jobs in different ways. Let’s explore.

The importance of partnerships

A quick note on the importance of partnerships: You’ll notice throughout the examples below that almost every one of them is accomplished via a partnership. With tech talent becoming harder to find, partnerships will be a key strategy to bridge the talent gap and implement complex technology at scale—and quickly.

The future of claims: Replace and augment

To address the workforce gap in claims, technology will be used to both replace and augment employees, though the scale of this impact will be different between personal and commercial lines.

Personal:

Personal claims is the most prone to automation, especially for simple claims. A small parking lot car accident is a perfect example of an easy type of claim that AI can handle—with human spot-checking, of course.

Real-life tech example: Hippo recently partnered with Claimatic and Five Sigma to use automation to process homeowners’ claims faster and manage them end-to-end. From a customer perspective, this offers a single point of contact, faster response times and easier claims tracking. From an operations perspective, this automation reduces back-end friction and ensures accuracy by identifying the severity of a claim and flagging when a loss is identified.

Employee impact: There will likely be an employee scale-down of the claims workforce as automation manages more of the claims process. At the same time, remaining employees will be augmented with technology to help them to manage claims faster and more accurately. Looking at the Hippo example, part of its new automation technology is to match claimants with adjusters—a typically manual, time-consuming process. This augments the claims workforce so that they can avoid these types of administrative tasks and focus on what matters: the customer.

Commercial:

Like personal lines, commercial claims departments will be both replaced and augmented by cognitive technology, but at a different rate. Commercial claims are often more complex, so there will be more augmentation versus replacement, compared to personal lines.

Real-life tech example: Protective insurance partnered with Roots Automation to scale its trucking and commercial auto insurance claims. In only four months, Protective introduced two “digital co-workers” called Roxy (for sending letters to claimants) and Rex (for indexing claims documents). Both bots were able to complete 95% of tasks without human intervention.

Employee impact: Most claims employees working in commercial lines will be augmented by cognitive technology. The Protective insurance example shows how bots can be leveraged to manage the most time-consuming tasks, like indexing documents. This frees up employees to focus on more important tasks or handle more claims. This is especially important for the underserved small-to-medium business (SME) market. By streamlining commercial claims as much as possible, the SME market could look more attractive to insurers.

The future of underwriting: Augment

Underwriting encompasses both risk assessment and product development. This will continue to be a key area for insurers to remain modern and competitive, so headcount will likely not be cut. However, people are retiring. Insurers must ask themselves: Do we replace retiring workers or use technology to scale up our current workforce? With the current talent gap, that latter is more realistic. This means underwriting is moving into a world of semi-automation, both for personal and commercial lines. And that means re/upskilling.

Real-life tech example (personal): Product development is a huge part of underwriting, and a lot of insurers are leveraging cognitive technology to make the right products at the right time. Arbol partnered with RealTimeRental to offer real-time parametric weather protection for vacation rentals using AI, analytics and third-party data. AXA Life & Health Reinsurance Solutions uses a white-labeled version of Verisk’s Health Risk Rating Tool they’ve branded as the Intelligent Medical Acceptance Tool (IMPACT) to automate parts of the health insurance underwriting process to enable better coverage for customers with pre-existing conditions.

Real-life tech example (commercial): On the commercial side, risk is the core theme for cognitive technology. Allianz SE partnered with Cytora to tap into AI-based risk processing for its commercial lines business, allowing underwriters to focus on value-adding tasks. Another example is insurtech Neptune Flood, which developed an AI-based rating and quoting platform for automated risk assessment. With this technology, Neptune saw 400% growth and is now the largest private flood MGU in the US.

Employee impact: Technology is already changing underwriting, especially from a product development and risk assessment standpoint. Reskilling the workforce will be critical. Technology, in particular the ability to ingest third-party data leveraging the force of the cloud, can make product development fast and nimble. Workers will need to feel comfortable trusting new data sources and AI to drive innovation. Looking at risk assessment, a human perspective will always be important. But underwriters can be informed and supported by AI and other cognitive technology to improve accuracy and make better decisions. Employees will need to be reskilled to modernize their approach and take advantage of the large-scale analysis offered by AI and other technologies.

The future of sales: Augment and grow

It’s not surprising that sales and its associated functions, like marketing, will need to scale with digital tech. Sales will have to get more innovative as competition grows and customers demand a seamless experience. New areas, such as embedded insurance, will leverage technology and strategy in a way the industry has never done before. To support this rapid shift and growth, sales functions will need to expand while also being augmented with technology.

Real-life tech example (personal): Direct Auto & Life Insurance chose Marketing Evolution’s customer journey tracking solution. This persona-based marketing measurement and optimization platform will provide insights into the touchpoints customers engage with along their path to purchase. These insights will help Direct Auto & Life Insurance to better understand its customers, deliver a personalized experience and critically—how to link behavior to sales.

Real-life tech example (commercial): Nationwide expanded its relationship with Amazon Web Services to innovate and deploy innovative products while they also streamlined internal operations. From a sales commercial perspective, this partnership helped Nationwide build a Small Business Advisory platform that uses machine learning to tailor personalized insurance policy recommendations to small business customers in minutes.

Employee impact: Sales, marketing and customer engagement are critical for growth. Employees in these areas will be augmented with technology, while teams expand headcount. To remain competitive, insurers will need to innovate and build a business development ecosystem. Technology by itself won’t do this. Like underwriting, cognitive technology will offer the tools for creative salespeople to innovate—and the customer insights to make data-driven decisions and promote growth.

Roadmap to the future: A cross-functional perspective

As I mentioned before, job functions don’t operate in silos. So, this breakdown gets more complicated when we look at how each function interacts with each other. For example: Claims and underwriting are intertwined. Modernizing claims to better leverage the data used in underwriting and vice versa is more important than ever. Breaking down these silos will drive an enterprise level change in behaviors and collaboration.

That’s why insurance companies need to take a cross-functional perspective when determining how technology will change their workforce. And this should not be a theoretical strategy.

How to use tech to close the insurance workforce gap

Insurers should put together a concrete workforce roadmap. The roadmap should be modular, outlining which areas will need new hires versus reskilling. It should consider the interaction between functions and how changing one will impact the other. It should also indicate where people can be moved around to capitalize on your current workforce and the knowledge and experience that they have.

Another key element of evolving your workforce is early inclusion. Employees deserve transparency when it comes to how their jobs will change. Early involvement will help employees feel like they are a part of that change—and minimize replacement fears. Because all the roadmaps in the world won’t help if employees feel threatened and reject change. Insurance companies can avoid this by being supportive, honest and by listening.

While a roadmap and transparency are important from an employee perspective, the technology side is its own domain. This blog looked at the product and service side of the insurance workforce, but implementing cognitive technologies requires a talented, motivated IT team. Insurers will need to marry a tech roadmap that aligns with its workforce vision using agile methodologies to allow for flexibility and pivots, if needed. Critically, executives need to be able to communicate this holistic vision across the organization—including tech partners.

The insurance industry has a tough road ahead when it comes to talent. Decades’ worth of knowledge is about to be lost to high retirements, and younger generations aren’t banging down the door to work in insurance. Carriers will need to get creative using a mix of technology and a reskilled human workforce to close this gap and drive future growth. The time for this transition is now, or else you risk falling behind. Just remember that employees are people—treat them with respect and compassion, and they will rise to your expectations. As we say at Accenture: Innovation happens where technology meets human ingenuity. The insurance industry will need both to succeed in the future.

Transforming claims and underwriting with AI: AI has emerged as the critical differentiator in the insurance industry when applied in tandem with humans.

Get the latest insurance industry insights, news, and research delivered straight to your inbox.

Disclaimer: This content is provided for general information purposes and is not intended to be used in place of consultation with our professional advisors.

Disclaimer: This document refers to marks owned by third parties. All such third-party marks are the property of their respective owners. No sponsorship, endorsement or approval of this content by the owners of such marks is intended, expressed or implied.

[ad_2]

Source link